Help centre

Your bank, financial institution or payment service provider will be able to help you with most of your PayTo queries. We have included the answers to some frequently asked questions here

PayTo is a modern digital payment solution offered by banks, financial institutions, and payment service providers in Australia. It has been developed by Australian Payments Plus in collaboration with the industry. Your bank, financial institution or payment service provider will be able to help you with most of your PayTo queries, however we’ve included the answers to some frequently asked questions here.

Support for consumers

About PayTo

What is PayTo?

PayTo is an easy way to authorise and control payments from your bank account. PayTo can be used in several ways. A couple of examples are; a digital alternative to direct debit, and allowing you to pay directly from your bank account where you previously needed a card (like for in-app purchases and online shopping).

How does PayTo work?

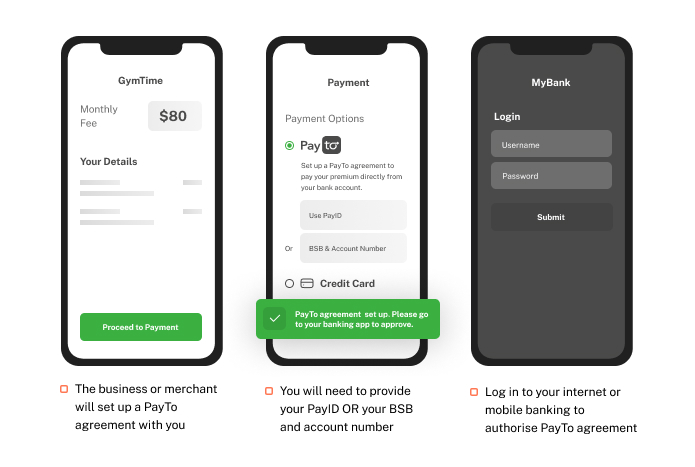

A business or merchant will set up a ‘PayTo agreement’ with you. This is where you authorise how much, and when, you will pay for goods or services. It could be for a one-off, ad-hoc, or recurring payment.

The PayTo agreement will appear in your internet or mobile banking app for your authorisation. Once you have authorised the agreement, the business can debit your account according to the terms that you have agreed.

Why should I use PayTo?

PayTo is an easy, secure payment option giving you more control over payments from your bank account.

You can see your PayTo agreements in your internet or mobile banking app, so you’ll know when payments will be debited from your account. You can pause, cancel and make certain changes to agreements there too.

PayTo also allows you to use your bank account directly for payments that previously needed a card. So now you just need your PayID, or BSB and account number – no need to remember card details and expiry dates!

When is PayTo going to be available?

PayTo is currently available in the online banking of over 50 banks, financial institutions and credit unions, with more to come. Look out for PayTo as a payment option offered by businesses and organisations.

Where will I see PayTo offered as a payment option?

PayTo is brand new and has started to become available as a payment option across businesses and organisations. As PayTo becomes more widely available, you’ll be able to use it for all kinds of payments. Some examples are recurring membership fees, in-app payments, online shopping, and utility bills. Keep your eye out for the PayTo logo.

What can I do if I want to use PayTo as a payment option, but my bank, building society or credit union does not offer PayTo yet?

Your bank, building society or credit union will let you know once PayTo is available.

Who owns PayTo?

PayTo is an initiative of NPP Australia, the organisation that operates Australia’s real-time payments infrastructure, the New Payments Platform (NPP). PayTo is developed by NPP Australia in collaboration with banks, fintechs and payment services providers.

NPP Australia is a wholly owned subsidiary of Australian Payments Plus, Australia’s domestic payment organisation that also includes BPAY Group and eftpos.

Is PayTo replacing direct debit?

Among other uses, PayTo may be used as a digital and more modern alternative to the current direct debit system. Some merchants and businesses will move their direct debits to PayTo to give customers a better customer experience with more visibility and control over their payments.

Who do I contact for help?

If you have a query about a PayTo agreement, you should first get in touch with the business or merchant. If they are not able to resolve your query, please get in touch with your bank, building society or credit union.

Safety & security

Is PayTo safe?

- PayTo is a safe way to use your bank account for payments because a PayTo agreement must first be authorised within your internet or mobile banking app. This means it is subject to the same level of security as the rest of your banking relationship. Until the agreement has been authorised, a payment cannot be made from your account.

- When a PayTo agreement is sent to your internet or mobile banking app for authorisation, you should check the details carefully and make sure it is in line with what you have agreed before authorising it.

- Once a PayTo agreement is authorised, the business or merchant can only debit your account in accordance with the payment terms that you have agreed to.

Is it safe to give a merchant or business my PayID or BSB and account number?

- In order to create a PayTo agreement with you, a business or merchant will need your BSB and account number, or better still, your PayID.

- The PayTo agreement will be sent to your internet or mobile banking app for your authorisation.

- Without your authorisation of the PayTo agreement, the merchant or business cannot debit your account.

- Once a PayTo agreement is authorised, the business or merchant can only debit your account in accordance with the payment terms that you have agreed to.

What if a payment is taken outside of the terms of my PayTo agreement?

- If you have a PayTo agreement with a business or merchant that has taken payment that you believe to be outside of the terms of the agreement, you should contact them to rectify it.

- As with any payment method, you should only be charged in line with your contractual agreement with a business or merchant.

- If you are unable to resolve your concern with the business or merchant, please contact your bank, building society or credit union for further assistance.

What if money is taken without my authorisation at all?

- If money is ever taken out of your account without your authorisation, you should contact your bank, building society or credit union immediately.

If the debit was made by a business with whom you are a customer, or have a relationship, you should contact the business to alert them and request it to be rectified.

Using PayTo

How do I use PayTo?

- When PayTo is the chosen payment method, the business or merchant will set up a PayTo agreement with you. This is where you agree how much, and when, you will pay them for goods or services. It could be a one-off, ad-hoc, or recurring payment.

- You will need to provide your BSB and account number, or your PayID.

- The PayTo agreement will then appear in your internet or mobile banking app for your authorisation. Once the agreement is authorised, the business or merchant will debit your account according to the terms that you agreed to.

What information do I need to give to the business or merchant?

To set up a PayTo agreement with a business or merchant, you will need to provide your PayID or your BSB and account number. The business will let you know any other details they will need.

Do I have to use a PayID or can I use my BSB and account number?

PayTo agreements can be created using either your PayID OR by using a BSB and account number. Most banks, building societies and credit unions offer PayID, and it saves you needing to remember your BSB and account number (or entering it correctly!).

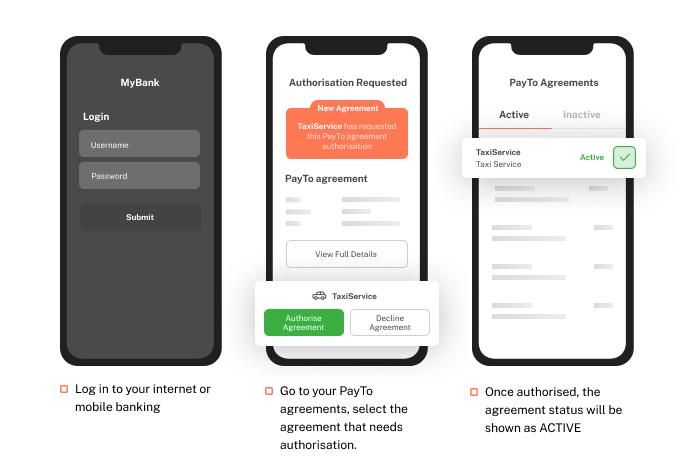

How do I authorise a PayTo agreement?

- Log in to your internet or mobile banking app.

- Find the section where your bank displays your PayTo agreements. A PayTo agreement that needs your approval will be marked as “Pending authorisation”.

- Once you click on the PayTo agreement, the payment terms will be displayed for you to check.

- If you are ready to authorise it, click ‘Approve’. The agreement will then be marked as ‘Active’.

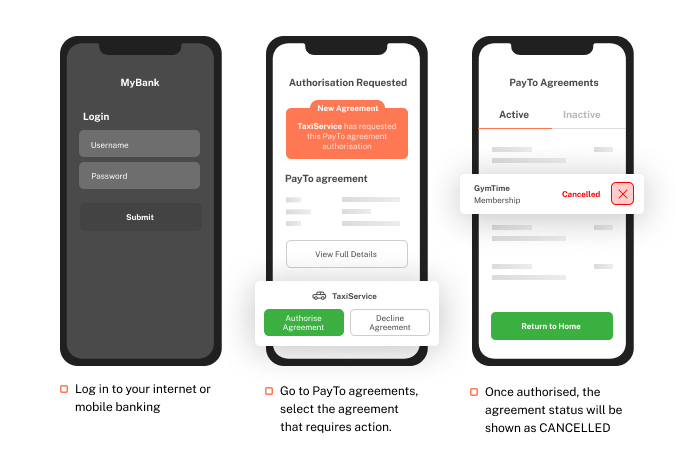

How do I decline a PayTo agreement?

- Log in to your internet or mobile banking app.

- Find the section where your bank displays your PayTo agreements. A PayTo agreement that needs your approval will be marked as “Pending authorisation”.

- Once you click on the PayTo agreement, the payment terms will be displayed for you to check.

- If you do not want to authorise it, click ‘Decline’. The agreement will then be marked as ‘Cancelled’.

Please be aware that this doesn’t change your contractual arrangements with the business or merchant.

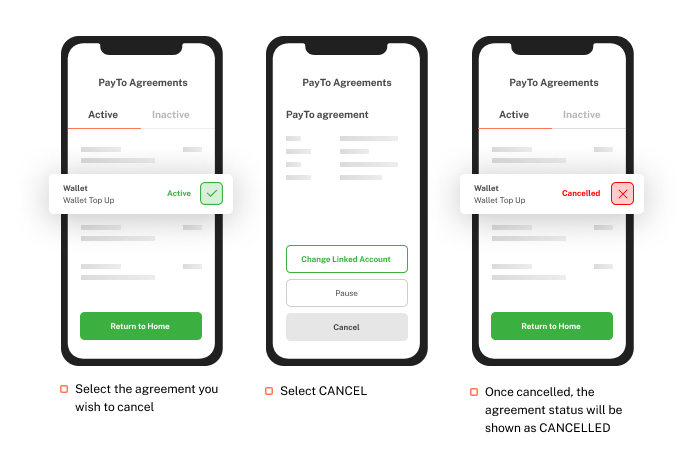

How do I cancel a PayTo agreement?

- Log in to your internet or mobile banking app.

- Find the section where your bank displays your PayTo agreements.

- Click on the PayTo agreement that you wish to cancel and the detailed PayTo agreement will be shown.

- Click ‘Cancel’. The agreement will then be marked as ‘Cancelled’.

Please be aware that this doesn’t change your contractual arrangements with the business or merchant.

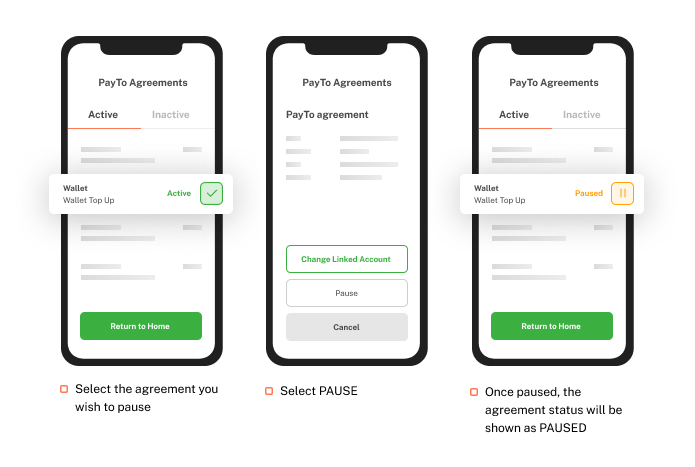

How do I pause a PayTo agreement?

- Log in to your internet or mobile banking app.

- Find the section where your bank displays your PayTo agreements.

- Click on the PayTo agreement that you wish to pause and the detailed PayTo agreement will be shown.

- Click ‘Pause’. The agreement will then be marked as ‘Paused’.

Please be aware that this doesn’t change your contractual arrangements with the merchant.

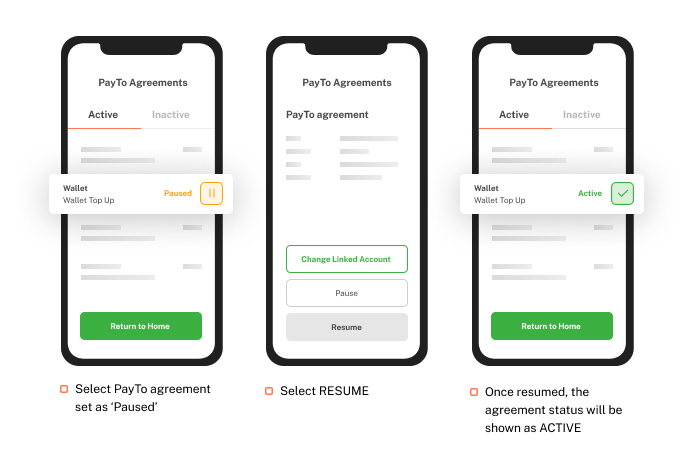

How do I resume a PayTo agreement after I paused it?

- Log in to your internet or mobile banking app.

- Find the section where your bank displays your PayTo agreements.

- Click on the PayTo agreement that you wish to resume and the detailed PayTo agreement will be shown.

- Click ‘Resume’. The agreement will then be marked as ‘Active’. The business or merchant will then be able to debit your account according to the terms that you have authorised.

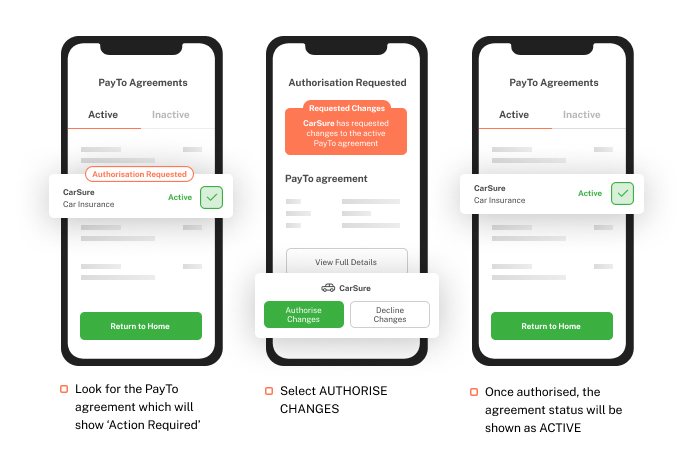

How do I reauthorise a PayTo agreement after the merchant made changes?

- Log in to your internet or mobile banking app.

- Find the section where your bank displays your PayTo agreements.

- A PayTo agreement that needs your approval will be marked as “Pending authorisation”.

- Once you click on the PayTo agreement, the revised payment terms will be displayed for you to check.

- If you are ready to authorise it, click ‘Approve’. The agreement will then be marked as ‘Active’.

PayTo agreements

What is a PayTo agreement?

A ‘PayTo agreement’ is a payment agreement between you and a business or merchant where you agree how much, and when, you will pay them for goods or services. It could be for a one-off, ad-hoc, or recurring payment.

Where do I find my PayTo agreements?

You can find your PayTo agreements in your internet or mobile banking app.

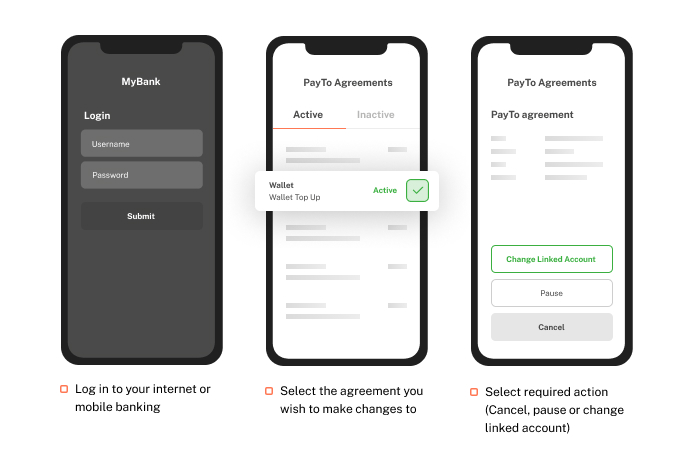

Can I make changes to an agreement?

You can find your PayTo agreements in your internet or mobile banking app. Here, you can also pause or stop your PayTo agreements, or even change the linked bank account.

Please note that pausing or cancelling a PayTo agreement doesn’t change your contractual arrangements with a business or merchant.

For changes to the payment amount or frequency, the business or merchant will need to make the change. They will then send you an updated PayTo agreement for reauthorisation.

What should I look for when reviewing a PayTo agreement?

A PayTo agreement contains important details about how much, and when, you agree for your account to be debited for goods or services

It could be for a one-off, ad-hoc, or recurring payment.

You should check that this information matches what you have agreed to with the merchant or business:

- Name of merchant or business

- Amount of the agreement, including any maximum amount (or cap)

- The payment terms which describe:

- When your payments will be made, including starting and ending dates

- Payment frequency (how often your payments will be made)

- Payment number (how many payments, if instalments, will be made)

What if I don’t agree with the PayTo agreement?

If you do not wish to proceed with the PayTo agreement, you can select ‘decline’. Please note that declining an agreement does not change any contractual agreement you have with the business or merchant.

What do I do if the details of the PayTo agreement are wrong?

If you find the details in the PayTo agreement are not in line with your agreement with the merchant or business, you should decline it and contact them. They will cancel the incorrect PayTo agreement and create a new, correct one for your authorisation.

PayTo availability

Why doesn’t my bank account work for PayTo?

PayTo is currently available in the online banking of over 50 banks, financial institutions and credit unions, with more to come.

Why can’t I see PayTo anywhere as a payment option?

PayTo is brand new and has started to become available as a payment option across businesses and organisations. As PayTo becomes more widely available, you’ll be able to use it for all kinds of payments. Some examples are recurring membership fees, in-app payments, online shopping, and utility bills. Keep your eye out for the PayTo logo.

Moving from direct debit to PayTo

What should I do if my direct debit is moving to PayTo?

Some businesses will move direct debit arrangements to PayTo because it is a digital and more efficient way to manage recurring payments. PayTo will allow you to be able to see and control these payments securely in your internet or mobile banking app.

If you have a direct debit arrangement that is moving to PayTo, you don’t need to do anything. This is the process you can expect:

- You will first receive 14 days’ advance notice from the business or merchant of its intended move to PayTo.

- Once the ‘direct debit request’ has been moved to a ‘PayTo agreement’, you will then be able to see and control it within your banking app.

- This PayTo agreement doesn’t need to be re-approved as you have already authorised the existing direct debit request with the business or merchant.

Finally, once the PayTo agreement is in your banking app, the business will allow 5 days before debiting your account.

Why would I want my direct debit to move to PayTo?

PayTo offers a simple, digital experience that gives you more visibility and control over payments. You can see and manage PayTo agreements securely in your internet or mobile banking app.

Do I have to agree to move my direct debit to PayTo?

No. The business or merchant will give you 14 days’ advance notice. During this notice period, you may choose to ‘opt out’ and remain on the current direct debit system.

How do I stop my direct debit moving to PayTo?

To opt-out of your direct debit request moving to PayTo, you need to contact your merchant or business to see what other payment options are available to you.

If you need help

The details in my PayTo agreement are wrong

When a PayTo agreement is presented in your internet or mobile banking app for authorisation, you should carefully check all the details and payment terms. If something is not correct, you can decline it, and notify the business or merchant so that they can set up a correct one.

I did not receive the PayTo agreement in my banking app

Check that you have provided the merchant or business with your correct PayID, or BSB and account number. If it is correct, and not appearing in your internet or mobile banking app, you should contact the merchant or business to help. If they cannot assist you, then please get in touch with your bank, building society or credit union.

An unauthorised payment was taken from my account, and I have not been able to resolve it with the merchant or business.

If payment was taken outside of the terms of your PayTo agreement, you should first get in touch with the merchant or business to allow them to rectify it.

If you have attempted to resolve it with the merchant or business and it remains unresolved, please contact your bank, building society or credit union.

I think my account has been accessed fraudulently as there are payments and/ or PayTo agreements that I do not recognise.

If you suspect that your account has been used fraudulently, you should contact your bank, building society or credit union immediately. It’s also worth checking if a business you have recently interacted with uses a different formal business name for banking than the trading name you are familiar with.

I used PayTo to pay for goods and/ or services that I am not satisfied with.

If you have used PayTo to purchase goods or pay for services that you are unhappy with, you should contact the merchant or business.

If your concern is not resolved, you should explore avenues of consumer protections that are offered under Australian law. The Australian Competitor & Consumer Commission (ACCC) outlines consumers rights and guarantees and provides useful information and tools on its website here: https://www.accc.gov.au/consumers

Support for merchants and businesses

About PayTo

What is PayTo?

PayTo is a new, digital way for merchants and businesses to initiate real-time payments from customers’ bank accounts.

Why should I offer PayTo as a payment method for my customers?

PayTo offers real-time, reliable payments to help businesses run a little bit smoother:

- Remove the uncertainty of receiving payments from bank accounts with real-time account validation, funds verification, and notifications at various stages of payment

- See when a payment agreement is paused, changed, or cancelled, allowing you to build better customer relationships

- Reduce the chance of dishonours, disputes and exception processing

How does PayTo work?

Your business will set up a ‘PayTo agreement’ with your customer. This is where you agree how much, and when, they authorise you to debit their account. It could be for a one-off, ad-hoc, or recurring payment.

The PayTo agreement will be sent to your customer’s bank, building society or credit union and will be presented in their internet or mobile banking app for authorisation.

Once the customer has authorised the agreement you can start debiting their account in accordance with the agreed payment terms.

What can my business use PayTo for?

PayTo supports a broad range of use cases. These include a modern alternative to direct debt, a digital payment solution for in-app and ecommerce transactions, more efficient business processes like outsourced payroll and accounts payable and the payment of eInvoices. PayTo can also be used along with QR codes to develop better customer experiences. More.

When can my business start using PayTo?

Businesses can start using PayTo now. Check if your financial institution or payment service provider can help you offer PayTo here.

Why would I offer PayTo when it’s only available to some customers now?

You can start using PayTo before all customer accounts are enabled. This will help start to integrate PayTo into your systems and processes.

If you are a direct debit user, there are significant benefits in moving direct debits to PayTo. Your PayTo Sponsor can help you identify which accounts you could begin with so you can get started.

How do I access PayTo?

For merchants and businesses to use PayTo to initiate real-time payments, they need to be sponsored as a PayTo User. Businesses should consult with their bank, financial institution or payment service provider to find out more about when their PayTo capabilities will become available. Once available, PayTo Sponsors provide access to PayTo through proprietary channels or services such as APIs. For information regarding which organisations offer PayTo services, please email info@nppa.com.au.

What is a PayTo User?

In order to use PayTo to initiate payments from customers’ bank accounts, a business needs to be sponsored as a PayTo User. A Sponsor could be any organisation that offers PayTo services such as a payment service provider, bank, or other financial institution.

Safety & security

Is PayTo safe?

Yes, PayTo is a safe way to initiate payments as a PayTo agreement must first be authorised by a customer within their internet or mobile banking app. This means you have confidence that the account is valid, and the customer has authorised the PayTo agreement themselves.

Using PayTo

How do I set up a PayTo agreement?

Once sponsored as a PayTo User, your business can set up PayTo agreements. Your sponsoring organisation will outline the steps required to set up a PayTo agreement.

What information do I need from the customer?

When offering PayTo as a payment option, you will need the customer’s BSB and account number, or PayID. Your PayTo sponsor will tell you what other information that you need to collect to set up a PayTo agreement.

What happens if a customer cancels a PayTo agreement?

PayTo gives customers more visibility and control over payments from their bank accounts. It also gives businesses and merchants visibility of changes made to agreements. If a customer cancels or pauses a PayTo agreement with you, you will receive notification of this.

If your customer is under a contractual agreement with you, you will need to contact them to arrange another payment method.

If your customer is not under a contractual agreement with you, you can use the opportunity to improve the customer relationship or experience.

How much does PayTo cost?

Please contact your sponsoring organisation to discuss commercial terms for access to PayTo.

Moving from direct debit to PayTo

How do I move direct debits over to PayTo?

To move direct debit arrangements over to PayTo, you will need to work with your sponsoring organisation. In accordance with the rules under which you have established the direct debit arrangement with your customer, you need to provide at least 14 days’ notice before a PayTo agreement is set up to replace a direct debit request. Once the PayTo agreement is set up, payments can be initiated 5 days later.

What if some customers don't have PayTo enabled with their bank yet?

As it will take some time for all retail banking customers’ accounts to be ready for PayTo, you may consider the benefits of commencing the move from direct debit to PayTo with those accounts which are ready earlier. Your sponsoring organisation can assist with this guidance.

Can customers decline moving to PayTo?

Yes, a customer may opt-out of the move to PayTo.

If a customer opts out of moving to PayTo withing the 14 day notice period, your existing arrangement stays in place.

What happens after the direct debit is set up in PayTo?

Once the direct debit has been moved to PayTo, your customer’s bank can check the arrangement details, and to liaise with the customer to confirm they are aware of the direct debit arrangement that has been moved to PayTo. After 5 (calendar) days, you may begin initiating payments against the PayTo agreement.

Is there an ideal time to move a customer’s direct debits to PayTo?

Ideally, you should attempt to move any direct debit arrangements to PayTo at least 5 days in advance of your next agreed collection/initiation date. This is because once a PayTo agreement has been presented in the customer’s internet or mobile banking app, a payment cannot be initiated for 5 days.

PayTo agreements

What if the customer doesn’t approve the PayTo agreement?

If the customer does not approve the PayTo agreement, you will not be able to debit their account. You will need to request the customer to approve the agreement, or to provide another payment option

How will I know if the customer has approved/ declined/ cancelled their PayTo agreement?

You will receive notification of changes to the status of a PayTo agreement. The form of this notification will be determined by your sponsoring organisation.

What happens if I have to change the payment details (e.g. increase the payment amount) of an existing PayTo agreement?

You can make changes to an existing agreement as often as you need. Please refer to your sponsor for more information on how to do this.

Where you make changes to the payment terms (e.g. increase an amount), your customer will be required to authorise that change before you will be able to initiate payments for the new amount.

If you need help

Where can I get more information on PayTo?

Please get in touch with your PayTo sponsoring organisation for more information or assistance with PayTo.

Am I liable for charges that a customer may dispute?

Payments may only be initiated in line with an authorised PayTo agreement. Please refer to your PayTo sponsoring organisation for more information on its dispute process.